- February 29, 2016

- Posted by: admin

- Category: Entity Formation and Taxation

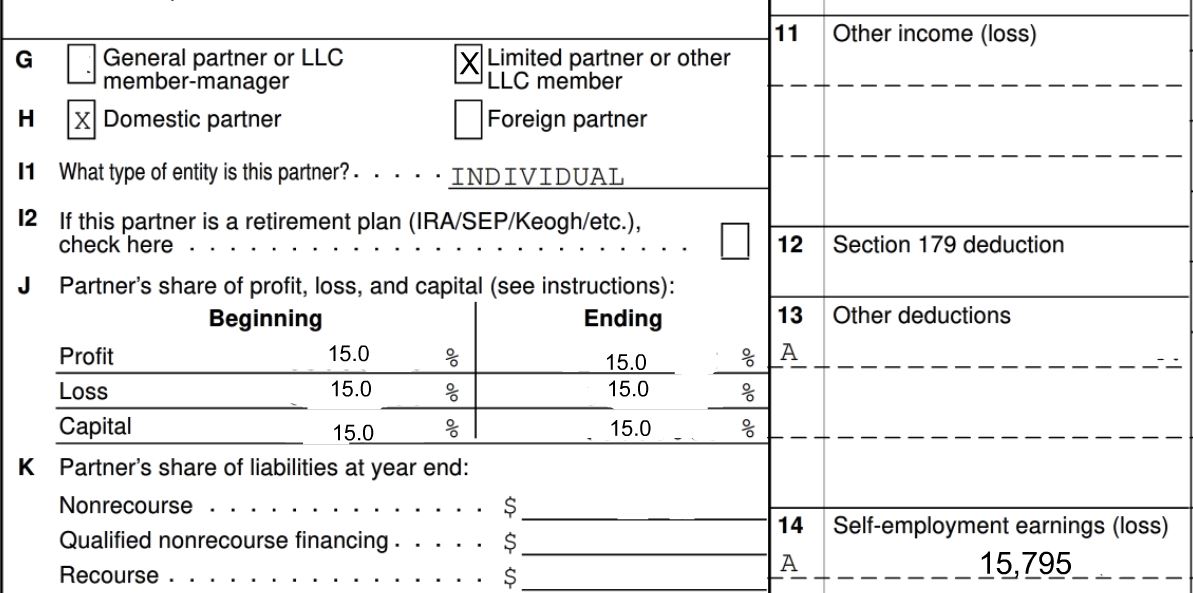

Since 1977, limited partners have reported distributive income as passive investment income not subject to self-employment tax. But the times they are a changin’. With the increased popularity of LLPs and LLCs, the IRS is looking more closely at the facts and circumstances, and less at the legal structures, of taxpayer and entity relationships.

There have been rumblings of clarification of the tax treatment of limited partner and LLC member income for SECA purposes, but Congress has made little progress. The IRS continues to decide the treatment of distributive income on a case-by-case basis, with no concrete guidance. The courts have consistently upheld that a passive activity under IRC Section 469 is not necessarily a passive activity under IRC Section 1402(a)(13).

If you are relying on your tiered entities to shelter you from SECA, you may be in for some sticker shock. My advice? Don’t rely on your K-1 to determine whether or not your income is subject to self-employment tax or ACA’s new investment tax . Discuss your entity relationships with your CPA to determine the proper reporting.

See also:

Federal Register / Vol. 62, No. 8 / Monday, January 13, 1997 / Proposed Rules